Today’s resource-challenged tax departments often find it necessary to focus on what’s most critical. Although the release of the Pillar Two model rules captured attention, its adoption remained uncertain until things abruptly changed at the end of 2022, when three events occurred:

- The European Union unanimously agreed to a directive mandating that member nations adopt Pillar Two by the end of 2023 with an income inclusion rule (IIR) effective in 2024. Since then, other countries have followed suit;

- The Organisation for Economic Co-operation and Development (OECD) released further guidance on transitional and, eventually, permanent safe harbor rules; and

- The OECD released revised guidance on a standardized global anti-base erosion (GloBE) information return (GIR) outlining a data structure and reporting format.

Timing remains in flux, but one thing is clear: the time to prioritize Pillar Two planning is now.

Minimize Disruption and Avoid Surprises

What do these developments mean for multinational enterprises (MNEs)? Those with constituent entities in jurisdictions that have adopted Pillar Two will need to account for its impact in their 2024 income tax provisions. If you don’t have a comprehensive plan in place to prepare, read on for a complete Pillar Two playbook detailing four parallel steps to take.

Step 1: Establish a Pillar Two Timeline

The Pillar Two process requires planning for a new set of calculations based on multiple jurisdictions. It will likely include reporting requirements that won’t fit neatly into existing work streams. Further, requirements are coming quickly at different levels of materiality and precision—and some jurisdictions will enact OECD rules in different ways. With no time to wait for definitive answers, MNEs should build processes as they deliver results.

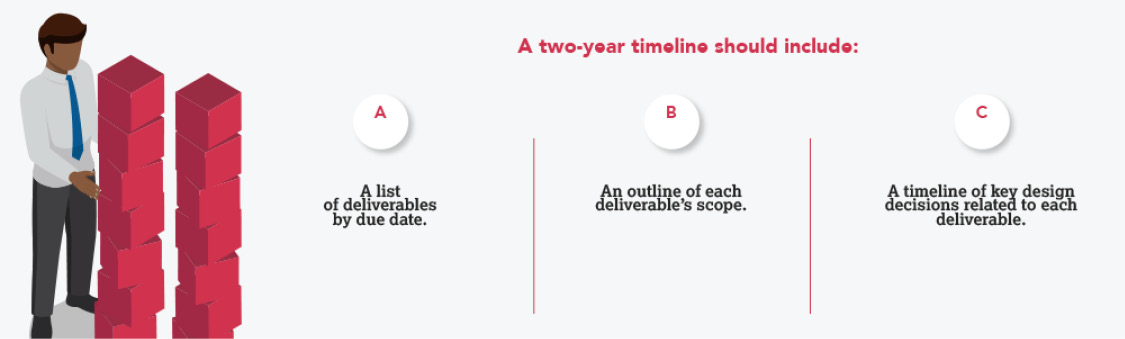

A two-year timeline should include the following stages:

A. List Deliverables by Due Date

Calendaring deliverables to meet external deadlines is key, but perhaps the more pressing concern is setting deadlines for deliverables that answer internal questions. Most immediately, management and other executive stakeholders need to understand potential global minimum tax (GMT) impacts, such as effects on effective tax rate (ETR) and exposure to additional cash tax outflows. Externally, even without defined deadlines or enacted laws, we can make certain assumptions about deliverables over the next two years and beyond. It’s probable that several jurisdictions will have enacted an IIR effective for 2024. A top-up tax and an IIR will be required from a tax accounting perspective starting with the first quarter of 2024. At the same time, many jurisdictions will implement a qualified domestic minimum top-up tax (QDMTT). A QDMTT will allow those jurisdictions to collect a top-up tax and avoid allocation of any part of the tax to foreign jurisdictions through an IIR or an undertaxed payments rule (UTPR). And by 2025, the compliance process must begin in a number of different jurisdictions.

B. Outline the Scope of Each Deliverable

Next, we should define how detailed our deliverables need to be. A high-level planning analysis requires less precision than what’s needed to book to financial statements. The level of detail for provision will be less than what is required for compliance in a GIR. Defining the desired breadth and granularity of the analysis will keep the project on track.

C. Make Key Design Decisions

In addition to establishing deadlines for internal and external deliverables, practitioners should create deadlines for what they need to analyze to best meet requirements. Beyond its complexity, Pillar Two presents unique challenges:

- It’s a completely new obligation that doesn’t leverage existing processes;

- It’s a moving target; and

- Jurisdictions will enact rules inconsistently.

Tax will need to make key design decisions to determine how Pillar Two will fit into the existing organizational structure. That process will evolve into 2025 as we get more clarity around rules and move from planning all the way to compliance.

The types of decisions and their potential outcomes will differ based on when they need to occur and for whom. For example, if you have only some weeks to provide a high-level risk analysis to management, you need to make quick decisions to answer questions such as:

- What data should be used for the initial analysis? Given the short timeline, granularity could interfere with meeting the deadline;

- Who should own the analysis? You may be limited to those people following OECD developments, who may not be the people who will own the process; and

- Which tools should be used for the analysis? You may arrive at a solution that changes over time. Decisions related to a high-level risk analysis will differ from, and perhaps be more urgent than, decisions needed to support tax accounting implications. And decisions around tax accounting may be different and more urgent than determinations around filing a GIR. It’s important to focus on the totality of what needs to be acted upon—and not just on the first, more reactive, set of decisions. Setting both a high-level work plan of deliverable due dates and a timeline for key decisions allows tax management to move forward at the same time they focus on the entire spectrum of considerations.

Step 2: Identify and Organize Data

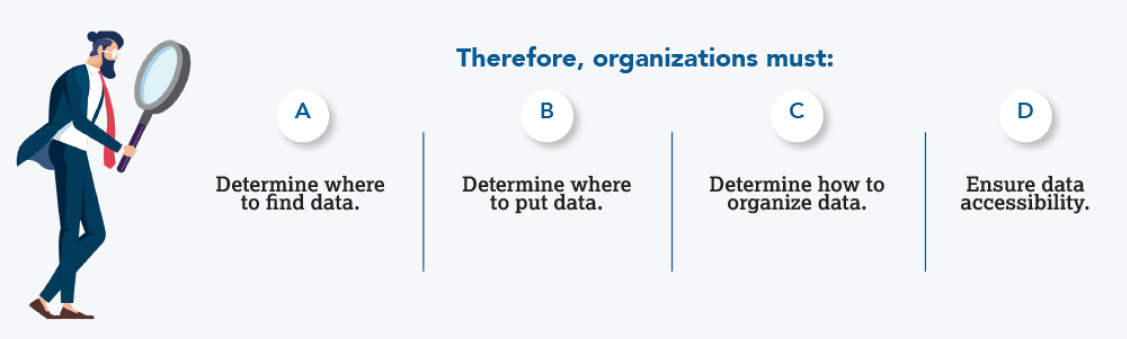

MNEs face significant decisions related to data at every stage of Pillar Two implementation. The current GIR reporting framework for tax administrations includes thousands of data points. Therefore, organizations must determine not only where to find the data (and if it’s even captured), but also how to store, organize, secure, and share it.

A. Determine Where to Find Data

The first question to ask: What data do I need? The OECD’s latest GIR draft identifies the data that global tax administrations will require when reviewing and auditing Pillar Two compliance.

Once we know the data we need, we can determine its source location. Start with the data you already have. A great deal of the data required for Pillar Two calculations can be found within financial trial balances needed for provision and compliance reporting. But is it at the right level? The best way to know is to build a data map or to leverage one your tax system has created. While we don’t yet have actual regulations from tax administrations for GloBE income and covered taxes components, we do have OECD model rules. The model rules define, article by article, both GloBE income and covered taxes, including exclusions and adjustments for both. A critical first step can be creating a data map that connects the organization’s trial balance, the article numbers, and the GIR data points.

After mapping from a financial account to the specific article number, we must determine if the data has the level of detail required by the model rules’ description of the component. In many cases, less detail may be required. For example, Article 3.2.1 of the model rules requires adjustments to GloBE income for certain equity-based transactions. In most circumstances, those transactions would not be identifiable at the account balance level. It would require digging into individual transactions for identifiers at the transaction level. A mapping to those identifiers could be applied consistently to automatically extract data needed to make the adjustments.

Some data won’t be in financial systems at all. Article 4.4 of the model rules allows for the impact of temporary differences—likely to be tracked within provision work papers and tools—to be included in covered taxes and reducing a potential top-up tax. However, the rules for included and excluded deferred taxes are extremely complex. Data related to the temporary differences will need to be mapped from its income tax supporting detail, rather than from the financial system itself. Changes may be required in how temporary difference reversals are stored and tracked within the provision system in order to be usable for Article 4.4 Covered Taxes.

Tax departments should undertake this analysis now as a crucial early step in Pillar Two preparation. Use the OECD guidelines to know where you will get the data you need to plan, calculate, and ultimately report any top-up tax and Pillar Two requirements.

B. Determine Where to Put Data

Knowing where to put data is as important as knowing where to source it. Storing data centrally—and having the ability to access and redeploy it—ensure a seamless process from planning through provision and compliance.

Looking back, many organizations didn’t adequately centralize data for country-by-country reporting (CbCR) and suffered complications as a result. At that time, the OECD provided guidance by releasing draft CbCR Tables 1 and 2, which identified data to include in reporting. Many organizations split responsibilities for handling that data among stakeholders. Transfer pricing teams focused on risk analysis at a detailed level, whereas compliance teams focused on populating data at the consolidated level for reporting.

Though both teams relied on the same data, they extracted it from individual silos instead of using the same data for their respective needs. Doing so not only created redundancies, but also increased the risk that reported data differed from analyzed data, a difference that would then require reconciliation. Teams could have stored large volumes of data in a common system to use for detailed risk analysis and reporting—and to aggregate for consolidated reporting.

Unfortunately, Pillar Two could easily head down a similar path. It’s more complex than CbCR because it includes an actual tax accrual. Plus, it’s more than just a reporting and risk exposure analysis. It contains risk, certainly, but includes a calculation of taxes across multiple jurisdictions involving different entities that will directly impact financial statements as early as the first quarter of 2024. Further, more processes are affected, meaning that more stakeholders will need to use and analyze the data.

As we also saw with CbCR, tax has a propensity to collect and use data directly within and throughout spreadsheets. Spreadsheets are a great place to use data but an ineffective place to store data for Pillar Two or, for that matter, any other process. Learning from CbCR pitfalls, tax should prioritize centralizing Pillar Two data in a common repository for use across functions and processes. Doing so will make data available to everyone who needs it and avoid process redundancies and reconciliations.

C. Determine How to Organize Data

In addition to finding the right data and strategically storing it, data should be easily accessible and make sense to all who require it. This is not unique to Pillar Two, but Pillar Two data presents challenges, both in complexity and the vast amounts needed from various sources for calculations. How does a stakeholder know which data to use and where to use it? The OECD model rules and GIR guidance provide a road map. But how can source data from multiple processes be integrated in a way that maintains its integrity and its traceability to its source? And how should it be presented to align with model rules?

Success means effectively creating a new tax base—yet another basis of accounting that tax will be responsible for maintaining. Most MNEs already do this, though perhaps inefficiently. For example, they maintain separate income tax bases for compliance and provision, they maintain a separate tax base by jurisdiction, and they track earnings and profits as a separate tax base.

In theory, Pillar Two should be just another layer. The difficulty comes from our past. Most tax departments are not set up to layer from one base to another without transferring data. Navigating the various iterations of IIR and UTPR across jurisdictions will require tax departments to build an ecosystem of tax bases centered around the OECD model rules and GIR. And, to complicate matters further, Pillar Two model rules and commentary provide guidance for two separate components that must be tracked individually, as follows:

1. GloBE Income

The first component is GloBE income. Using the structure of the GIR and applying model rule requirements, tax departments should create a new version of net income. Once tax has identified the source, the department needs to organize the data into a completely new trial balance with its own basis of accounting.

2. Covered Taxes

The second component, covered taxes, creates a variation on income tax provisioning. Taxpayers must take their current and deferred income tax expense and adjust it to create what amounts to an income tax expense under an entirely new accounting method.

D. Ensure Data Accessibility

The necessity for structure around Pillar Two data goes beyond its use in calculations. The underlying source data and calculated results must be shared across multiple processes, stakeholders, and reporting requirements. For reporting requirements, the tax department must implement a reporting structure that can access a multitude of data and summarize it into reviewable elements that include:

- safe harbors (transitional and permanent);

- GloBE income (adjusted);

- covered taxes;

- GloBE effective tax rate (ETR) by entity and by jurisdiction;

- substance-based income exclusion;

- top-up tax;

- qualified domestic minimum top-up tax (QDMTT);

- income inclusion rule (IIR); and

- undertaxed payments rule (UTPR).

For now, these reports reflect a set of model rules that could easily change as different jurisdictions implement their own laws. And that could change individual elements of the reporting. Local internal and external stakeholders need access to a centralized set of standard data for these individual reporting requirements.

Where to Put the Data?

Making data accessible means evaluating options for where to put it.

First, tax departments can build an in-house platform—a resource-intensive undertaking with a heavy cost for both development and maintenance.

Alternately, they can outsource data storage and maintenance to a third party. There may be benefits to a third party producing calculated results, as we discuss later. However, outsourcing data ownership and control presents a host of risks to the organization. For example, if you use multiple service providers, and each owns and maintains its own set of data, you risk losing consistency, and you add the need for additional reconciliation. Plus, your own people understand your data and have the best insights into the business—so they can contextualize findings better than a third party can.

Last, tax can implement a tax system that builds and maintains the calculations and reports. This will ensure that tax owns and controls the data and makes it available to internal and external stakeholders who need it—without introducing inconsistencies into the process.

Immediate Data Access: Additional Advantages

1. Relevant Analytics

Standardized reporting provides a direct path from source data through complex calculations, allowing users to reconcile and validate calculated results. Data cannot be available only to tax professionals involved in the calculations, however. Tax needs to tell a story of what results mean to those unfamiliar with them: how results could impact operations and where risk exists. The story needs to make findings understandable to those with little knowledge of underlying requirements. Those stakeholders must grasp how Pillar Two could affect the larger enterprise, including its financial statements, the amount of tax potentially paid to various jurisdictions, and more. To do this, tax must condense and visualize data to make it meaningful to nontax individuals.

2. Financial Reporting

Long before reporting for compliance purposes, calculation results need to be accessible to tax accounting and finance teams, quickly summarized for a journal entry, thorough enough for financial disclosures, and transparent enough for audit.

3. Compliance Reporting

Ultimately, the data needs to be transferred to tax administrations for compliance reporting. The most likely format for this reporting, the GIR, must be extracted and transmitted to multiple jurisdictions. It is highly likely that US MNEs will be subject to Pillar Two obligations in multiple countries. The reason is that the United States has not passed compliant Pillar Two legislation, without which the United States cedes its ability to collect top-up tax to other jurisdictions through an IIR or UTPR.

A centralized top-up tax will be allocated to different countries and reported in those countries. Data and reporting must be centralized globally at the organization’s tax headquarters, but they must also be accessed, analyzed, and reported at the local country level. This multi-jurisdictional, multi-stakeholder layer creates complexity in data access that goes beyond legacy processes. It also creates the need for our next two steps: building the right team and leveraging the right technology.

Step 3: Build the Right Team

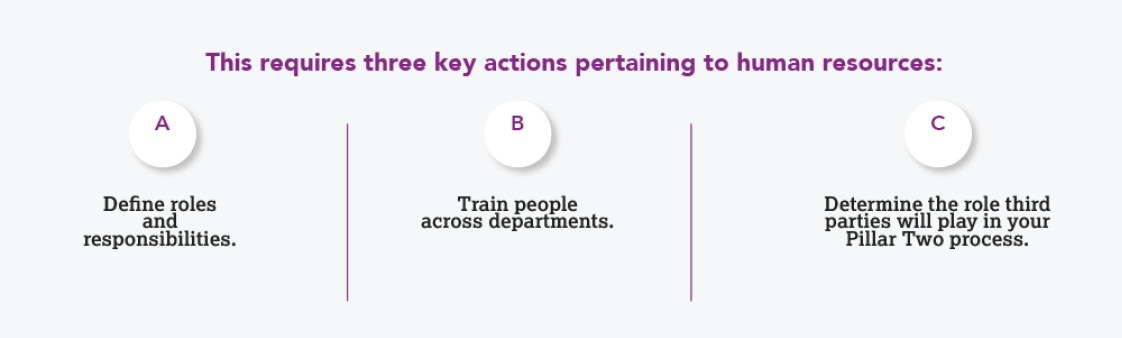

Creating a complete and automated data structure is only part of the plan. Tax departments must also ensure their people are prepared to understand Pillar Two’s impact on the organization and can meet its compliance and reporting requirements. This requires three key decisions pertaining to human resources, as follows.

A. Define Roles and Responsibilities

Implementing a completely new process calls for allocating resources to construct an entirely new team, identifying who is responsible for what, integrating that team within the tax organization, and training the enterprise on how Pillar Two fits into the tax life cycle. Very early on, tax needs to define roles and responsibilities by:

appointing the ultimate owner of Pillar Two;

identifying regional leaders and work streams; and

building a team within each work stream.

B. Train People

Any Pillar Two implementation plan should include a comprehensive training plan, with the following three steps.

1. Train the Pillar Two Team

The most obvious training involves technical training for assigned Pillar Two teams. In some ways, this is the easiest form of training thanks to the significant amount of material available. However, although the OECD’s model rules provide a fairly detailed framework, few local governments have finalized and enacted actual legislation. Until that occurs, training must be ongoing.

2. Train the Rest of Tax

Many other stakeholders within the tax department need to clearly comprehend Pillar Two’s impact on their own tax life cycle processes. The main processes affected are tax accounting and transfer pricing.

3. Train the Rest of the Organization

Tax also has to tell the story to the organization. The C-suite, finance, and investor relations, among others, won’t understand the complexity of the model rules and the components of the calculation. But they need to know and to communicate the possible effects on the business. To do that, tax has to give them a story in a way that works for them.

Tax also has a vested, practical interest in ensuring that the larger enterprise understands the implications of Pillar Two. The more executive management, finance, IT, and other stakeholders appreciate the urgency, scope, and complexity of Pillar Two, the more likely they will be to fund the infrastructure needed to support the new process, including resources and a robust tax technology system.

C. Determine the Role of Third Parties

For many tax departments, third parties could be integral to the Pillar Two process. It’s critical to determine third-party participation up front. They can be advisors or the primary producer of results via outsourcing. Here are some considerations for each.

1. Advisory

In many instances, a tax organization will rely on a third party to provide expert guidance in the Pillar Two process. This advisory function can be integral to defining Pillar Two roles and responsibilities. Early in the process, you should determine whether a third party will:

- participate up front and provide guidance on what the organization should do;

- provide oversight and validation during the process; and

- furnish ongoing risk analysis.

All of these roles can be valid and vital, but it is important to define a third party’s involvement at the beginning and include it in the build-out of the team and processes.

2. Outsourcing

Between a lack of available tax resources and a lack of Pillar Two expertise, some tax departments may rely on third parties to fill the role of preparers, particularly for compliance-related processes. Although outsourcing may present a viable alternative for managing Pillar Two, it does not negate the need to train employees, understand the issues, and tell the story. In fact, in some instances outsourcing could complicate the situation. For example:

- What is the geographic scope of the third party’s role? The cross-jurisdictional nature of Pillar Two creates a “herding cats” nightmare for tax organizations. Global coordination and local country technical expertise are needed. Deciding how best to use an outsourcing firm involves prioritizing one of these objectives. A large firm may provide the global reach necessary to coordinate Pillar Two across the world. But a local firm may have specialized knowledge of local laws and a closer relationship with local resources.

- Who owns review and approval? One advantage of outsourcing is the ability to leverage the expertise and scale of firms. But it is important for tax leadership to set clear guardrails around who owns the final product, and who is responsible for reviewing and approving the result from both compliance and reporting standpoints. For many MNEs, outsourcing may be a convenient short-term solution as the organization builds in-house expertise and infrastructure to handle the complex long-term requirements of Pillar Two.

- Who owns the data? The biggest obstacle to outsourcing any tax function is data. Where is it? Who owns it? Who controls it? Because so much of Pillar Two data, both incoming source data and outbound calculated results, has mutual dependencies with other tax processes, it is crucial for tax to maintain both ownership and control over its own data. If a department outsources Pillar Two compliance and reporting to a third party, it still should build an in-house technology solution that can house and maintain data required for Pillar Two in a way that allows the rest of the organization to access and use it. Although one aim of outsourcing is reducing costs, some savings could be negated by the cost of maintaining multiple sets of the same data and adding reconciliations to the process.

Step 4: Determine the Right Technology

Fundamental to a successful Pillar Two implementation is, without a doubt, tax technology. Often, technology is an afterthought when planning for a new tax requirement. It’s frequently left to individual teams to use what they’re most comfortable with—and that’s generally Microsoft Excel. Universally used by the tax community and widely understood, Excel gives people a sense of ownership and control. But, at the same time, it can seriously restrict scalability, flexibility, and agility.

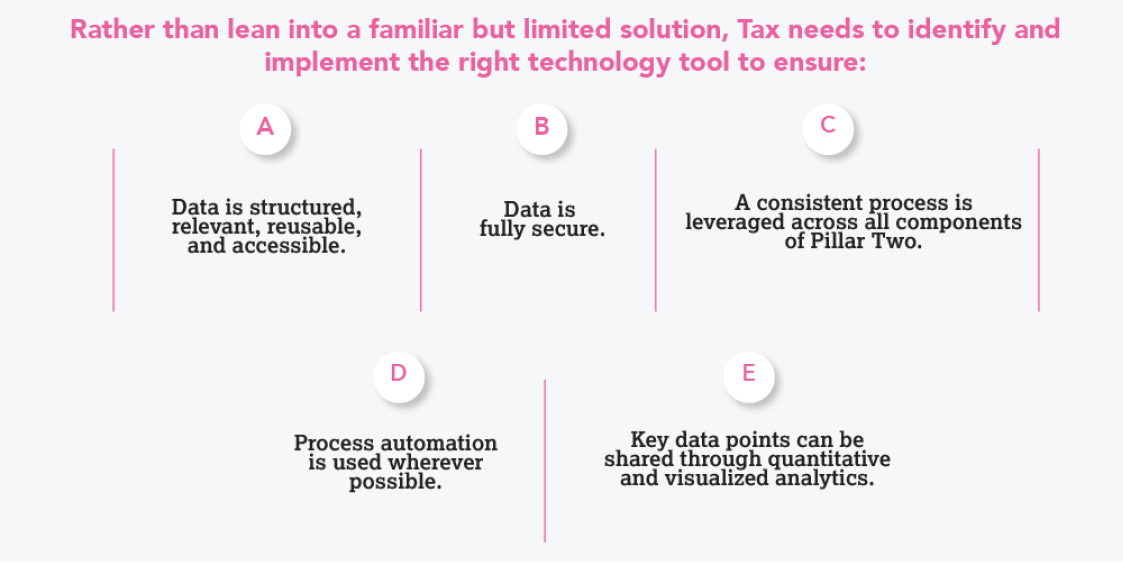

Rather than lean into a familiar but limited solution, tax needs to identify and implement the right technology tool to ensure the following processes are put in place.

A. Ensure Data Is Structured, Relevant, Reusable, and Accessible

Simply put, a database-driven technology solution is the only way to ensure data is stored in a structured way, relevant to Pillar Two calculations, reusable for multiple processes and purposes, and accessible to other stakeholders. Most of the data required for Pillar Two is redundant with data used in other tax processes including CbCR, provision, and income tax compliance. An ideal Pillar Two technology solution should use the same data across all processes in the tax life cycle. It should not require reimporting, rekeying, or moving data from one tool to another. Spreadsheets that require links and copying and pasting to move data, or disparate systems that shuffle data from one place to another, add layers of unnecessary reconciliation and risk.

For example, in designing the CSC Corptax Global Minimum Tax solution (Corptax GMT), Corptax added a layer of metadata by mapping the trial balance used for provision and compliance to an entirely new set of accounts based on Pillar Two model rules and the GIR. This allows the same trial balance to be used for all three processes without the need to move and reconcile it. The calculated IIR and UTPR top-up taxes are saved and used in the provision. Ideally, all processes should look to the same data—and the database should be relational enough—to include the metadata for a variety of processes.

B. Secure the Data

Data needs to be accessible yet secure. Your technology solution should include several levels of security.

- Huge volumes of sensitive data must be securely stored and its access limited to authorized users—a natural outcome of a structured tax system. The volume of Pillar Two data alone may easily overwhelm Excel, and user permissions are more difficult to establish and maintain in Excel.

- Security needs to control who can touch data—and when they can touch it. Technology offers control over functional access and supports the defined roles and responsibilities of the Pillar Two team.

C. Leverage a Consistent Process Across All Components of Pillar Two

The global Pillar Two team should be supported by a common global technology platform. Individual local teams often manage their calculations and obligations with technology tools that can’t talk to other technology tools. This makes it difficult to maintain a standard set of data and even harder to consolidate results into a global analysis. But the OECD model rules provide an opportunity for tax to implement a single set of calculations and reports globally.

D. Automate as Much as Possible

A sustainable technology platform for Pillar Two should automate:

- data collection from source systems and other tax processes;

- determination of GloBE income, exclusions, and adjustments;

- applicability of transitional and/or permanent safe harbor tests;

- calculation of covered taxes, including revaluing deferreds and the exclusion or recapture of unreversed temporary differences;

- calculation of top-up tax;

- allocations of IIR and UTPR;

- determination of QDMTT; and

- conversion of data into filing schemas for transmission to taxing authorities.

Historically, tax organizations often underuse the full capacity of their tax system—and use it to support offline manual compilations of data and results. The complexity and global reach of Pillar Two will require much greater reliance on automation.

E. Share Key Data Points Through Quantitative and Visualized Analytics

As a complete Pillar Two solution, the right partner can use large volumes of data to perform detailed calculations by country, organize the results into detailed reports for review, and condense those results into visual analytics that translate and illustrate impacts in charts and reports understandable to people outside of tax. Those analytics also give tax professionals a mechanism to understand the relationship between the organization’s structure and its source data—and how Pillar Two policies determine causation and trends.

Conclusion: Pulling It All Together

Pillar Two is an inevitable global tax obligation for MNEs. Tax organizations should immediately plan for its impact and implement a scalable, sustainable global tax process to address it. Take action now to:

- establish a plan that spells out the scope of deliverables and sets due dates for implementation;

- build a data structure that: 1) identifies source financial and tax data; 2) organizes data following the OECD GIR to facilitate calculations, reporting, and analytics; and 3) makes data accessible to internal and external stakeholders and extracts it for transmission to taxing authorities;

- build and train a global team that includes a worldwide headquarters-based owner, regional leaders, local compliance teams; and

- implement a technology platform that supports structured, standardized, and common data; secures data; supports automated Pillar Two calculations and reporting; and helps organizations tell the story of potential Pillar Two impacts.

Data and people are the drivers of a long-term, best-practice Pillar Two process. A proven global technology platform is the engine that gives tax organizations the tools to make it happen.

Gary Colbert is a senior director on the tax law analyst team at CSC Corptax.